Introduction

Whether you are looking to consolidate high-interest credit card debt, fund a home renovation, or cover an unexpected medical expense, a personal loan can be a powerful financial tool. Unlike a mortgage or an auto loan, a personal loan is typically “unsecured,” meaning you don’t need to put up collateral like your house or car. However, because there is no collateral, lenders are much stricter about who they approve. In 2026, getting the best rates requires a clean credit profile and a smart application strategy.

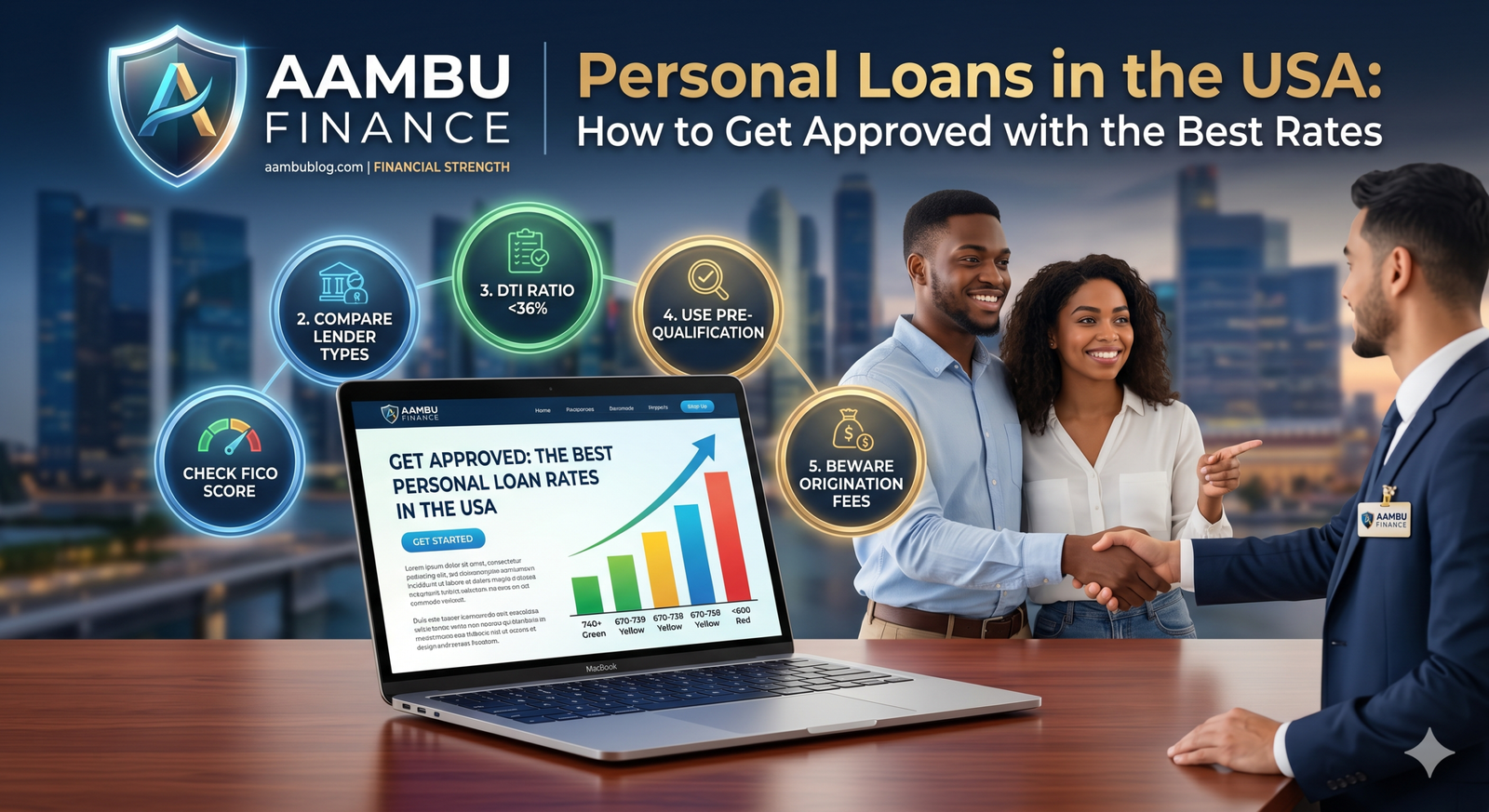

How to Secure the Best Personal Loan Rates

1. Know Your Credit Score: Your credit score is the #1 factor determining your interest rate (APR).

- Pro Tip: Borrowers with a score above 740 will qualify for the lowest “advertised” rates (often under 8-10%). If your score is below 600, you may face rates as high as 30% or more. Check your score on AAMBU FINANCE before applying.

2. Compare Different Lender Types: Don’t just walk into your local bank. In 2026, you have three main options:

- Traditional Banks: Best for existing customers with excellent credit.

- Credit Unions: Often offer lower rates and more personalized service.

- Online Lenders: (Like SoFi or Marcus) Faster approval times and great for competitive rates.

3. Watch Your Debt-to-Income (DTI) Ratio: Lenders look at how much of your monthly income goes toward debt payments.

- The Goal: Keep your DTI ratio below 36%. If your monthly debt payments (rent, car, credit cards) take up more than half your income, lenders will see you as high-risk and deny your application.

4. Check for “Pre-Qualification”: Many online lenders allow you to “Pre-Qualify” with a Soft Credit Pull. This lets you see the interest rate and loan amount you qualify for without hurting your credit score. Only agree to the formal application once you find a rate you like.

5. Beware of Origination Fees: Some lenders offer a low interest rate but charge a hidden Origination Fee (1% to 6% of the loan amount). Always look at the APR, not just the interest rate, as the APR includes these fees.

Conclusion

A personal loan is a commitment that should be taken seriously. By comparing lenders, keeping your DTI low, and protecting your credit score, you can secure a loan that helps your financial situation rather than hurting it. Always have a clear repayment plan before you sign the dotted line.

Frequently Asked Questions (FAQs)

Q1. What is the average personal loan interest rate in 2026? Answer: Rates vary wildly based on credit. Excellent credit borrowers may see 7-12%, while fair credit borrowers might see 18-28%.

Q2. Can I get a personal loan with “Bad Credit”? Answer: Yes, but it will be expensive. You may need a Co-signer with better credit to help you get approved or secure a lower rate.

Q3. How long does it take to get the money? Answer: Online lenders can often fund your account within 24 to 48 hours. Traditional banks may take 3 to 7 business days.

Q4. Is there a penalty for paying off the loan early? Answer: Most modern personal loans do not have Prepayment Penalties, but always check the fine print to be sure. Paying early saves you money on interest!

Q5. Can I use a personal loan to start a business? Answer: Yes, most personal loans have “no restrictions” on use. However, some lenders may have specific rules against using funds for business or gambling.