Introduction

Selecting your first credit card is a major financial milestone in the United States. It’s not just a payment tool; it is the foundation of your financial future. A well-chosen card helps you build a strong credit score, which is essential for renting an apartment, buying a car, or getting a mortgage. However, with thousands of options, picking the wrong one can lead to high fees and debt. Here is how to choose wisely in 2026.

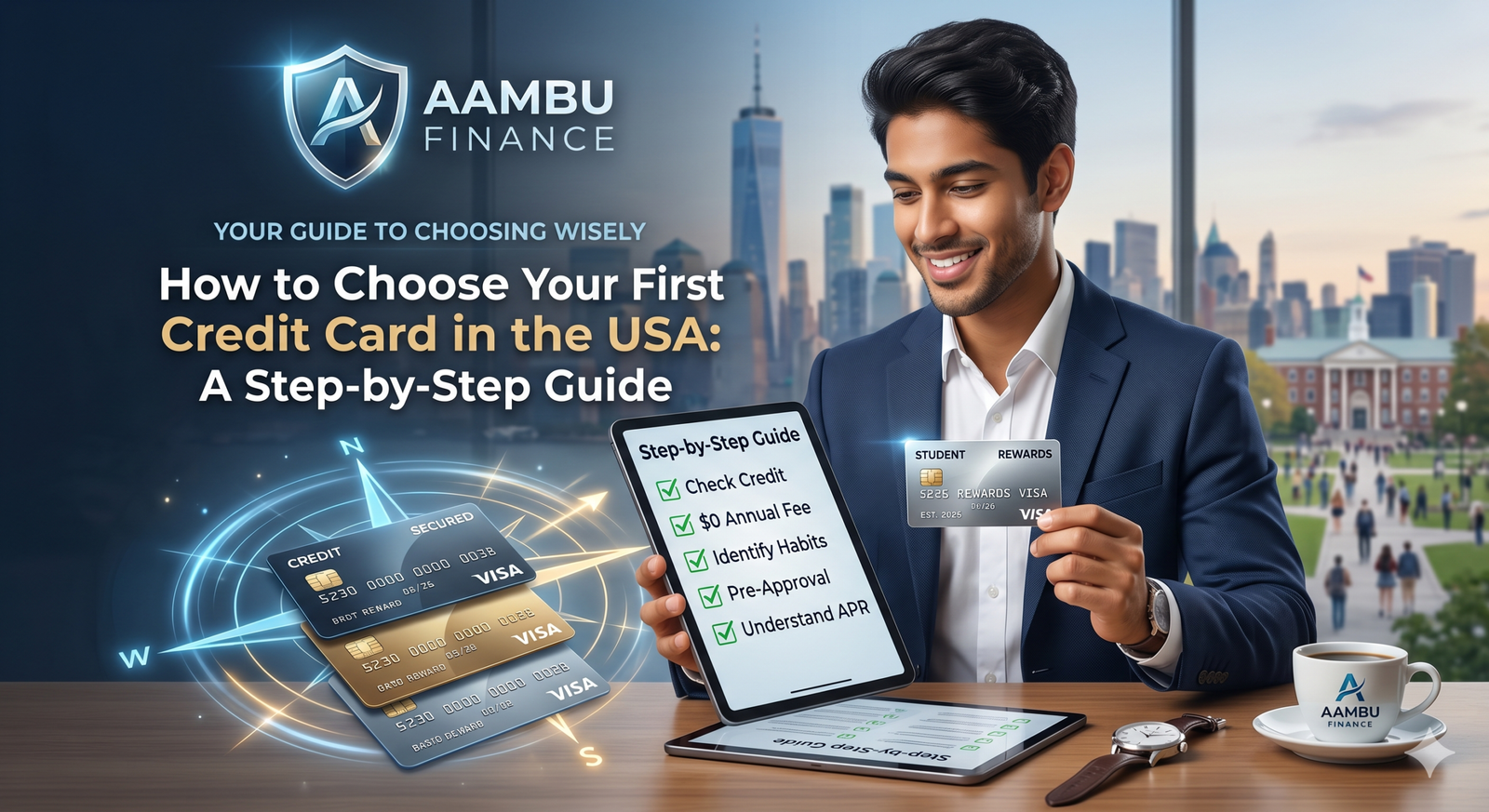

Step-by-Step Guide to Picking the Right Card

- Check Your Credit Standing First: If you have no credit history at all, you won’t qualify for “Premium” rewards cards. Look specifically for “Student Credit Cards” or “Secured Credit Cards.” A secured card requires a cash deposit that serves as your credit limit.

- Prioritize $0 Annual Fee: As a beginner, you should never pay a fee just to own the card. Since this will be your oldest account, you’ll want to keep it open for decades to build credit age. A no-annual-fee card makes this easy and free.

- Identify Your Spending Habits: Do you spend more on groceries, gas, or dining out? Choose a card that offers at least 1-2% cashback in those categories. This is literally free money back in your pocket.

- Look for “Pre-Approval” Offers: Before applying, use the “Pre-Approval” tools on bank websites (like Capital One or Discover). This allows you to see your chances of approval without a “Hard Inquiry,” which protects your score.

- Understand the Interest Rate (APR): While the goal is to pay your balance in full every month to avoid interest, it is still wise to choose a card with a competitive APR in case of emergencies.

Conclusion

Your first credit card is a training tool. The goal isn’t to get the biggest rewards, but to learn how to manage credit responsibly. By choosing a card with no annual fee and reporting to all three credit bureaus, you are setting yourself up for long-term financial success.

Frequently Asked Questions (FAQs)

Q1. What is the difference between a Secured and Unsecured card? Answer: A secured card requires a cash deposit (e.g., $200) as collateral. An unsecured card does not require a deposit and is granted based on your creditworthiness.

Q2. Does a first credit card have a low limit? Answer: Yes, typically first-time cards have limits between $300 and $1,000. As you show responsible behavior, the bank will automatically increase your limit.

Q3. How long should I wait before applying for a second card? Answer: It is best to wait at least 6 to 12 months after getting your first card. This gives you time to build a solid payment history.

Q4. Can international students in the USA get a credit card? Answer: Yes! Many banks offer cards to international students without a Social Security Number (SSN) if they have a valid passport and I-20 form.

Q5. Will my score go up immediately after getting the card? Answer: Your score will take about 6 months of consistent use and on-time payments to be officially calculated and start increasing.