Introduction

In the USA, your credit score is the summary, but your Credit Report is the detailed story. Lenders don’t just look at your three-digit number; they dive deep into your report to see your history of borrowing and repaying. However, most people find credit reports confusing and full of jargon. In 2026, understanding this document is the best way to catch identity theft early and ensure your financial health. Here is how to decode it like a pro.

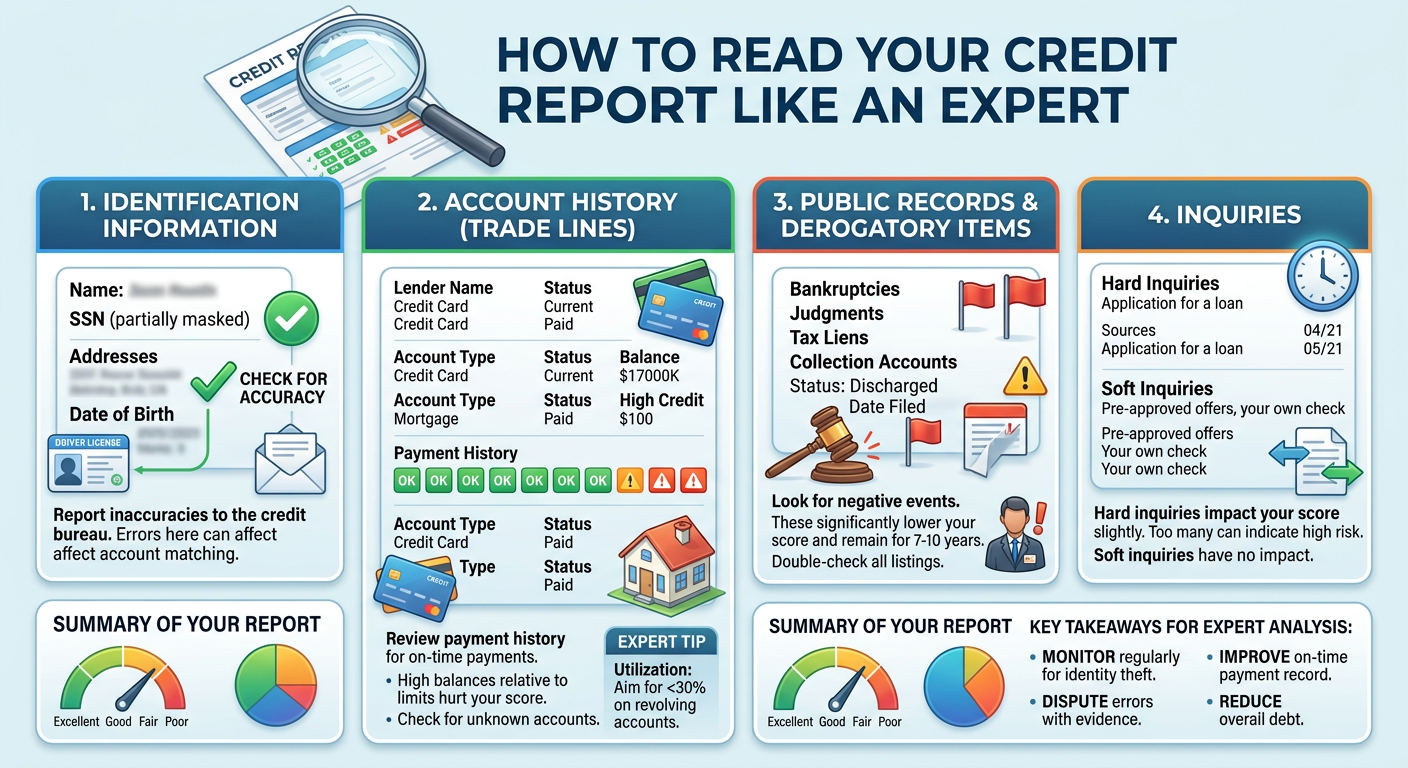

The 4 Main Sections of Your Credit Report

1. Personal Information: This section contains your name, current and previous addresses, Social Security Number (SSN), and employer history.

- What to check: Ensure there are no variations of your name or addresses you’ve never lived at. This is often the first sign of identity theft.

2. Account History (Trade Lines): This is the “meat” of the report. It lists every credit card, mortgage, and auto loan you’ve ever had.

- Look for: The “Account Status.” It should ideally say “Current” or “Paid as Agreed.” If you see “Late 30 days” or “Charged off,” these are the red flags hurting your score.

3. Public Records & Collections: This section lists legal items like bankruptcies or accounts that have gone to a collection agency.

- The Goal: You want this section to be Empty. Negative items here can stay on your report for 7 to 10 years.

4. Credit Inquiries: Every time you apply for credit, a “Hard Inquiry” is recorded here.

- Pro Tip: Check for inquiries from companies you don’t recognize. If someone tried to open a card in your name, it will show up here first.

How to Get Your Report for Free

Under Federal Law, you are entitled to a free credit report from each of the three major bureaus (Experian, Equifax, and TransUnion) every year. The only official website to get this is AnnualCreditReport.com.

Conclusion

Reading your credit report once a month is just as important as checking your bank balance. By understanding each section, you can spot errors, track your progress, and ensure that your financial reputation remains spotless in the eyes of lenders.

Frequently Asked Questions (FAQs)

Q1. Does my credit report show my criminal record? Answer: No. Credit reports only track financial data. They do not include criminal history, medical records, or political affiliations.

Q2. What should I do if I find an error? Answer: You must file a formal Dispute with the credit bureau that issued the report. They are legally required to investigate and respond within 30 days.

Q3. How long does negative information stay on my report? Answer: Most negative items (late payments, collections) stay for 7 years. Bankruptcies can stay for up to 10 years.

Q4. Does my credit report show my bank account balance? Answer: No. It shows your credit card limits and balances, but it does not show how much money you have in your checking or savings accounts.

Q5. Are the reports from all three bureaus exactly the same? Answer: Not always. Some lenders only report to one or two bureaus, so your Experian report might look slightly different from your TransUnion report.