Introduction

Many people in the USA check their credit scores daily on apps like Credit Karma or through their bank, but few actually understand the “Formula” behind that number. Why did your score drop 15 points after you paid off a loan? Why is it not moving even though you pay your bills? To master your finances, you must understand the five pillars that the FICO model uses to calculate your creditworthiness.

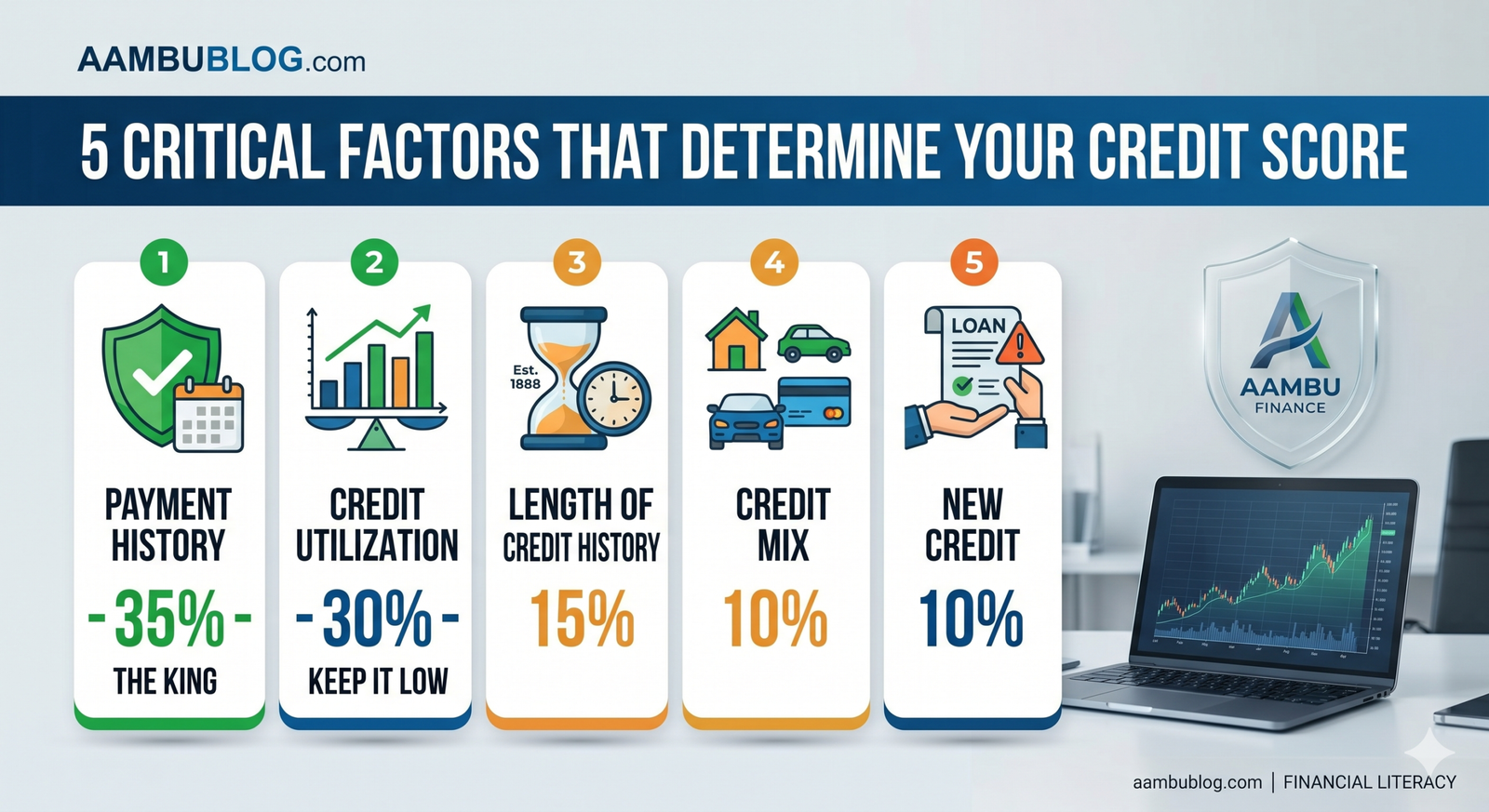

The FICO Formula: How Your Score is Calculated

Your FICO score is not a random number; it is a weighted calculation based on your credit report. Here are the five factors that matter:

1. Payment History (35%) — The King of Factors

This is the most significant part of your score. Lenders want to know one thing: Do you pay your bills on time?

- The Impact: Even a single late payment (30+ days) can stay on your report for 7 years and knock 50-100 points off your score instantly.

- Pro Tip: Always set up “Auto-Pay” for at least the minimum balance.

2. Credit Utilization (30%) — The Debt-to-Limit Ratio

This looks at how much of your available credit you are using. If you have a $10,000 limit and a $9,000 balance, your utilization is 90%, which is a huge red flag.

- The Impact: High utilization suggests you are overextended and struggling with cash flow.

- Pro Tip: For a top-tier score, keep your utilization below 10%, and never go above 30%.

3. Length of Credit History (15%)

Time is your friend. This factor considers how long your accounts have been open, including the age of your oldest account, your newest account, and the average age of all accounts.

- Pro Tip: Never close your oldest credit card account, even if you don’t use it. Closing it will shorten your credit history and hurt your score.

4. Credit Mix (10%)

Lenders like to see that you can handle different types of debt. A healthy mix includes “Revolving Credit” (Credit Cards) and “Installment Loans” (Car loans, Mortgages, or Student loans).

- The Impact: While not as critical as payments, having only credit cards can limit your score potential.

5. New Credit (10%)

Every time you apply for a new loan or card, a “Hard Inquiry” is placed on your report. Opening too many accounts in a short period makes you look “credit hungry” and risky.

- Pro Tip: Space out your credit applications by at least 6 months.

Summary Table: Weightage of Factors

| Factor | Weightage | Importance |

| Payment History | 35% | Extremely High |

| Amounts Owed (Utilization) | 30% | Very High |

| Length of Credit History | 15% | Medium |

| Credit Mix | 10% | Low |

| New Credit | 10% | Low |

Frequently Asked Questions (FAQs)

Q1. Does my income affect my credit score?

Answer: No. Your salary or bank balance is not a factor in your credit score. However, lenders look at your income separately to decide your “Ability to Pay.”

Q2. How long do Hard Inquiries stay on my report?

Answer: Hard inquiries stay on your report for 2 years, but they usually only affect your score for the first 12 months.

Q3. If I pay off my total balance every month, does utilization still matter?

Answer: Yes. The balance reported to the credit bureau is usually the balance on your “Statement Closing Date.” If that balance is high, your utilization will look high, even if you pay it off a few days later.

Q4. Can checking my score lower it?

Answer: No. Checking your own score is a Soft Inquiry. Only applications for new credit (Hard Inquiries) can lower your score.

Q5. Why did my score drop after paying off a loan?

Answer: This happens because you closed an “Installment Account,” which might have changed your Credit Mix or lowered the Average Age of your accounts. It is usually a temporary drop.